Thursday, July 2nd, 2015

by GEORGE BOLLENBACHER

Let me begin by saying that I believe the all-important swaps reporting requirement has been badly mishandled by the regulators worldwide, missing a golden opportunity to shed some light on this otherwise opaque market. In the US, one of the nagging problems has been that the SEC hadn’t put out its reporting rules, so there was no required reporting on one of the riskiest areas of the market – single-name CDSs.

Recently the SEC took a major step in rectifying this, by issuing some proposed and final rules. So, how well did they do? Let’s take a look.

Actually, the SEC issued three rules, two final and one proposed, which means that we will have to patchthem together to get as complete a picture as we can. The final reporting rule is: Regulation SBSR-Reporting and Dissemination of Security-Based Swap Information. There is also a proposed rule with an identical name, indicating that it will be combined with the final reporting rule at some point. I will cover both of them first. The SDR rule, Security-Based Swap Data Repository Registration, Duties, and Core Principles, I will cover later.

Including their preambles, these three rules comprise over 1,350 double-spaced pages. My practice has always been to go right to the rule text, since that is what everyone will be bound by, and then read any sections of the preambles that provide necessary clarifications. The rules themselves comprise 92 pages, a significantly more manageable reading assignment. I’ll cover only the unexpected or potentially troublesome aspects, but people should read all 92 pages.

In the SEC rulebook, the reporting rules are §§242.900-242.909.

Specifically:

242.900 Definitions

242.901 Reporting obligations.

242.902 Public dissemination of transaction reports.

242.903 Coded information.

242.904 Operating hours of registered security-based swap data repositories.

242.905 Correction of errors in security-based swap information.

242.906 Other duties of participants.

242.907 Policies and procedures of registered security-based swap data repositories.

242.908 Cross-border matters.

242.909 Registration of security-based swap data repository as a securities information processor.

Definitions

There are a few oddities among the definitions, each perhaps a warning about other oddities later on. One is “Trader ID means the [Unique Identification Code] UIC assigned to a natural per- son who executes one or more security-based swaps on behalf of a direct counterparty.” So that seems to be leading to a requirement to identify the person who executed the trade. Unless, of course, the trade was executed by a computer. Do we use HAL’s UIC then? There is also “Trading desk ID means the UIC as- signed to the trading desk of a participant,” and “Trading desk means, with respect to a counterparty, the smallest discrete unit of organization of the participant that purchases or sells security-based swaps for the account of the participant or an affiliate thereof.” So will we be identifying both the desk and the trader who did every trade? That’s not required anywhere else, and it certainly looks like overkill.

Who Reports?

Under the reporting obligations, we find another oddity:

(a) Assigning reporting duties. A security-based swap, including a security-based swap that results from the allocation, termination, novation, or assignment of another security-based swap, shall be reported as follows:

(1) [Reserved].

It looks like we are missing an important section. Sure enough, we find it in the proposed rule:

(1) Platform-executed security-based swaps that will be submit- ted to clearing. If a security-based swap is executed on a plat- form and will be submitted to clearing, the platform on which the transaction was executed shall report to a registered security- based swap data repository the information required. (emphasis added)

And one more item in the proposed rule:

(i) Clearing transactions. For a clearing transaction, the reporting side is the registered clearing agency.

I think that means that the SEF reports the original trade, and the DCO immediately reports the cleared trade. What about lifecycle events for cleared swaps? Here the final rule says:

(i) Generally. A life cycle event, and any adjustment due to a life cycle event, that results in a change to information previously reported … shall be reported by the reporting side, except that the reporting side shall not report whether or not a security-based swap has been accepted for clearing.

(ii) [Reserved]

Back to the proposed rule:

(ii) Acceptance for clearing. A registered clearing agency shall report whether or not it has accepted a security-based swap for clearing.

So, if the reporting side of the original trade is the SEF, and the DCO reports that it accepted the trade for clearing, does the DCO report the life-cycle events of cleared swaps? That should be the case, but the rules are a bit confusing about that.

What Transactions Must be Reported?

This is obviously a crucial question, and the final rule says:

(1) A security-based swap shall be subject to regulatory reporting and public dissemination if:

(i) There is a direct or indirect counterparty that is a U.S. person on either or both sides of the transaction; or

(ii) The security-based swap is accepted for clearing by a clearing agency having its principal place of business in the United States. (emphasis added)

And an indirect counterparty is defined as:

Indirect counterparty means a guarantor of a direct counterparty’s performance of any obligation under a security-based swap such that the direct counterparty on the other side can exercise rights of recourse against the indirect counterparty in connection with the security-based swap; for these purposes a direct counterparty has rights of recourse against a guarantor on the other side if the direct counterparty has a conditional or unconditional legally enforceable right, in whole or in part, to receive payments from, or otherwise collect from, the guarantor in connection with the security-based swap.

So a swap done between, for example, an EU dealer and a guaranteed EU subsidiary of a US corporation is reportable in the US, as well as by both parties in Europe. How fun! And who reports in the US? Back to §242.901.

In addition, the final rule requires reporting of all swaps in existence on the rule’s effective date (called backloading), and, al- though there is a phase-in for the rule as a whole, there doesn’t appear to be a phase-in period for backloading.

What Data Has to be Reported?

Here, in addition to the usual transaction material, the final rule requires:

(2) As applicable, the branch ID, broker ID, execution agent ID, trader ID, and trading desk ID of the direct counterparty on the reporting side;

Since only one side is reporting under the SEC rule, in dealer-to- dealer trades this appears to mean that the reporting dealer must supply all this information, but not the non-reporting dealer. What that accomplishes I’m not sure. Or else the reporting side reports all this internal information for the non-reporter.

There’s one other data requirement in this section:

(5) To the extent not provided pursuant to paragraph (c) or other provisions of this paragraph (d), any additional data elements included in the agreement between the counterparties that are necessary for a person to determine the market value of the transaction;

Thus it appears that the reporting party must determine what data is necessary for an outside entity to price the transaction, and include that if it’s not already delineated.

Public Availability

This section requires immediate public availability of the usual information (i.e., no identification of the parties) with this exception:

(3) Any information regarding a security-based swap reported pursuant to § 242.901(i); And 242.901(i), in the proposed rule, says,

(i) Clearing transactions. For a clearing transaction, the re- porting side is the registered clearing agency that is a counter- party to the transaction.

Does this mean that cleared trades are reported but aren’t publicly available? If so, what is the logic for that? If not, what does it mean? Beats me.

Other Factors

There is a significant section in the final rule called § 240.901A, covering reports the Commission is expecting from the staff “regarding the establishment of block thresholds and reporting delays.” The Commission will use these reports to determine “(i) … what constitutes a large notional security-based swap transaction (block trade) for particular markets and contracts; and (ii) the appropriate time delay for reporting large notional security-based swap trans- actions (block trades) to the public.” One of the considerations the rule highlights is “potential relationships between observed reporting delays and the incidence and cost of hedging large trades in the security-based swap market, and whether these relationships differ for interdealer trades and dealer to customer trades.” So block sizes and block reporting delays haven’t been decided yet.

Finally, the final rule defers the compliance dates to the pro- posed rule, and although the rule itself doesn’t say, the preamble lists two phases.

Compliance Date 1 – Proposed Compliance Date 1 relates to the regulatory reporting of newly executed security-based swaps as well pre-enactment and transitional security-based swaps.

One of the considerations the rule called

§ 240.901A highlights is “potential relationships between observed reporting delays and the incidence and cost of hedging large trades in the security-based swap market, and whether these relationships differ for interdealer trades and dealer to customer trades.”

On the date six months after the first registered SDR that accepts reports of security-based swaps in a particular asset class commences operations as a registered SDR, persons with a duty to report security-based swaps under Regulation SBSR would be required to report all newly executed security-based swaps… Registered SDRs would not be required to publicly disseminate any transaction reports until Compliance Date 2.

Compliance Date 2 – Within nine months after the first registered SDR … commences operations … (i.e., three months after Compliance Date 1), each registered SDR in that asset class … would be required to comply with Rules 902 (regarding public dissemination), 904(d) (requiring dissemination of transaction re- ports held in queue during normal or special closing hours), and 905 (with respect to public dissemination of corrected transaction reports) for all security-based swaps in that asset class—except for “covered cross-border transactions,”

So, six months from sometime for reporting, and nine months for public disclosure. That covers the SEC’s final and proposed rules on transaction reporting by market participants.

The SDR Rule

Now let’s look at the final rule on SDRs, and make some observations on the effectiveness of current and future reporting regimes.

The SEC’s final SDR rule is entitled “Security-Based Swap Data Repository Registration, Duties, and Core Principles” and runs some 468 pages. Don’t worry, you don’t have to read them all, just go to page 424 to find the beginning of the rule text. The bulk of the rule is in §232.13, which itself is divided into 12 subsections:

240.13n-1 Registration of security-based swap data repository.

240.13n-2 Withdrawal from registration; revocation and cancel- lation.

240.13n-3 Registration of successor to registered security-based swap data repository.

240.13n-4 Duties and core principles of security-based swap data repository.

240.13n-5 Data collection and maintenance.

240.13n-6 Automated systems.

240.13n-7 Recordkeeping of security-based swap data repository.

240.13n-8 Reports to be provided to the Commission.

240.13n-9 Privacy requirements of security-based swap data repository.

240.13n-10 Disclosure requirements of security-based swap data repository.

240.13n-11 Chief compliance officer of security-based swap data repository; compliance reports and financial reports.

240.13n-12 Exemption from requirements governing security- based swap data repositories for certain non-U.S. persons.

The Boring Stuff

As we can see from the list above, the first three sections of the rule pertain to registration as an SDR, or, as the SEC abbreviates it, SBSDR (except that they very seldom abbreviate it). Given that SDRs have been functioning in the US for more than a year, it would be astonishing if the SEC had significantly different registration requirements from the CFTC’s, and it doesn’t. So 13n-1 through 13n-3, 13n-6 through 13n-8, and 13n-11 are pretty much as expected.

Items of Interest

In light of the recognized problems with reporting accuracy, the following wording in 13n-4 bears examination:

(b) Duties. To be registered, and maintain registration, as a security-based swap data repository, a security-based swap data repository shall:

(7) At such time and in such manner as may be directed by the Commission, establish automated systems for monitoring, screening, and analyzing security-based swap data;

13n-5 has similar wording:

(i) Every security-based swap data repository shall establish, maintain, and enforce written policies and procedures reasonably designed for the reporting of complete and accurate transaction data to the security-based swap data repository and shall accept all transaction data that is reported in accordance with such policies and procedures.

So far, none of the US regulators have mandated any responsibility on the part of the SDRs to monitor data quality, nor have they laid out any guidelines for doing so. However, there are signs that such monitoring may be in the offing, and this language lays that responsibility squarely on the SBSDR. How extensive the monitoring might be, how the regulators would verify that it was being done, and what the penalties would be for failing in this function aren’t covered here. And, since 13n-4 is the only place in the rule text where the term “monitoring” is used, it isn’t covered anywhere else in the rule or, as it turns out, in the preamble.

The Current State of Affairs

In January, 2014 the CFTC issued a proposed rule called “Review of Swap Data Recordkeeping and Reporting Requirements.” The comment period ended May 27, 2014. I haven’t been able to find any comment letters on this proposal on the CFTC’s web site, nor any final rule on this subject.

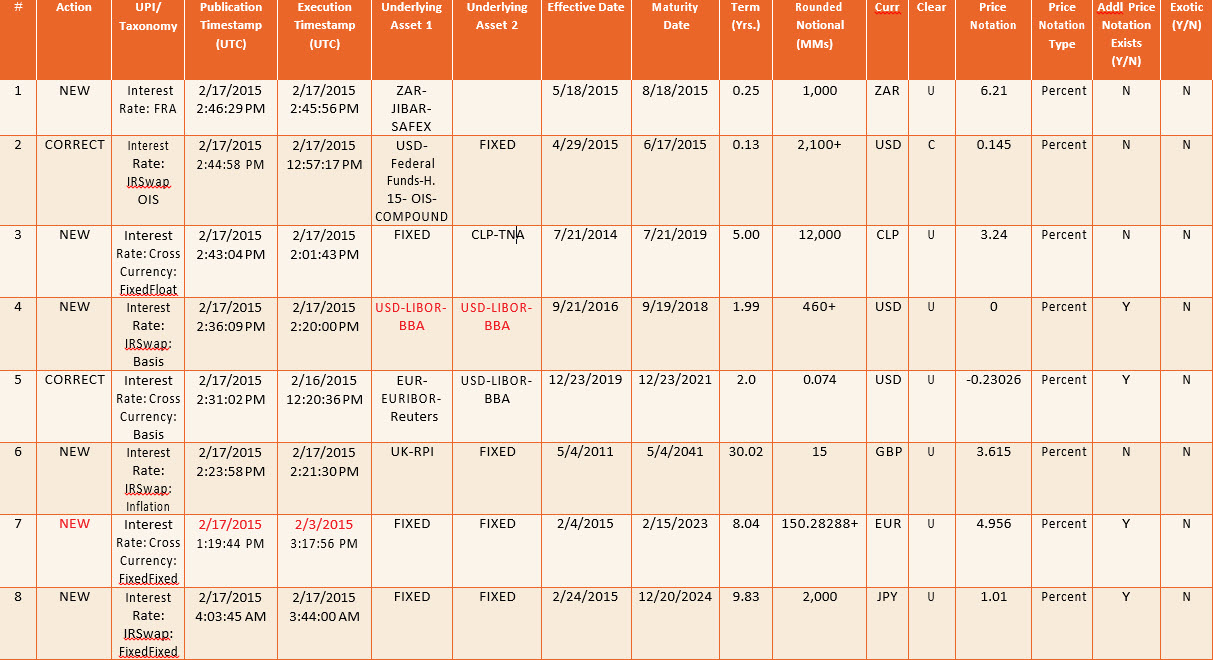

So how accurate is swaps reporting today? I took a look at a snapshot of the most liquid swaps category, rates, from the DTCC SDR site, and posted it below. The questionable items are in red.

Just to help us read the table, the first item is a new un-cleared ZAR three-month forward rate agreement beginning 5/18 and ending 8/18. The notional amount appears to be ZAR1,000,000,000 and the rate is 6.12%. With that as background, let’s look at some of the anomalies.

Item 4 is a new two-year USD basis swap beginning 9/21/2016. A basis swap is normally between two different floating rates, but the underlying assets in this transaction appear to be the same (USD-LIBOR-BBA). I’m not sure what a basis swap between the same rate would be, unless it is between two different term rates, like 1-year and 5-year. However, if that’s true the report doesn’t tell us, so we are in the dark as to what this trade really is.

Item 7 is a new 8-year Euro-denominated fixed-fixed above the block threshold (that’s what the plus at the end of the notional means) which appears to have gone unreported for two weeks. There is a delay in reporting block trades, but it isn’t two weeks. One of the monitoring functions the regulators might implement is any trade where the difference between the execution and reporting timestamps is greater than the rule allows.

Given the long delay between the CFTC’s reporting rules and these, we might expect that there would have been considerable communication between the agencies, and there might have been. It does appear that the CFTC is totally re-examining its reporting rules, and that might be a good thing.

Item 13 is a new 12-year Euro-denominated fixed-floating swap that appears to be above the block threshold of €110,000,000. What is interesting here is that the 12-year Euro rate at the time was about 0.4%, not 0.824%. If there is no other parameter on this trade, it looks to be significantly off the market, unless there was a large credit risk component.

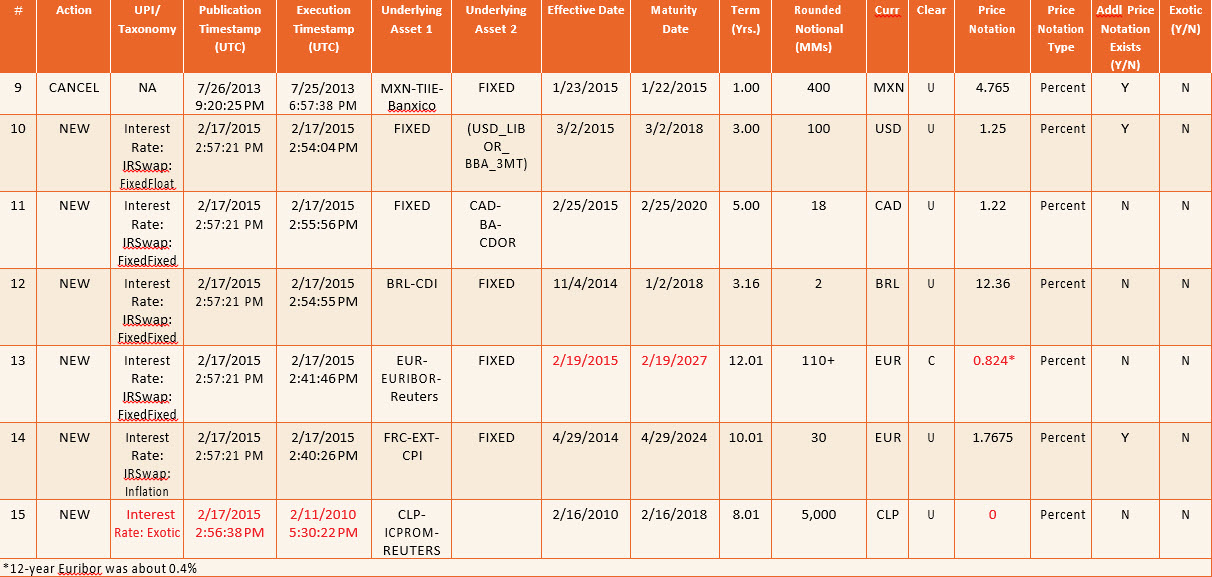

Item 15 is…what, exactly? It’s a new trade in some exotic that went unreported for 5 days, with no price given, apparently. Since the notional looks like 5,000,000,000 Chilean pesos, or about

$8,000,000, perhaps we don’t need to worry too much about what it really is, but exotics of this size denominated in dollars should cause us to ask just what kind of swap was done, and how much risk it entails.

Summing Up

Given the long delay between the CFTC’s reporting rules and these, we might expect that there would have been considerable communication between the agencies, and there might have been. It does appear that the CFTC is totally re-examining its report- ing rules, and that might be a good thing. Meanwhile, as firms get ready to report SEC-regulated swaps, the situation still looks pretty muddy. It might get better, but I’m not very optimistic about that.